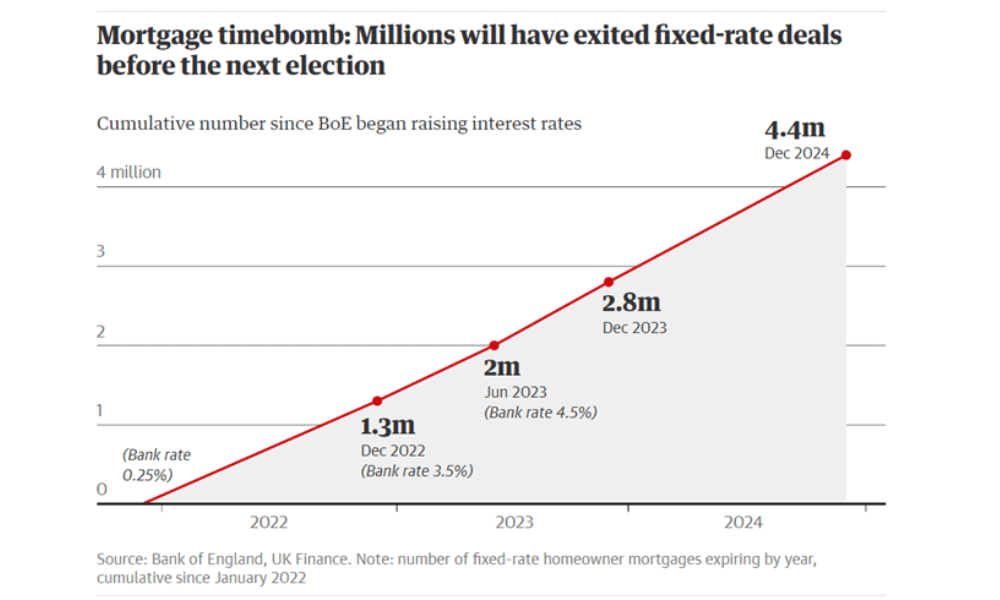

Over the course of the last 24 months, The Bank of England base rate has increased from 0.25% to 5.25% to control inflation – which peaked at 11% in 2022. For context, this jump represents the sharpest rise in interest rates in the 26 year history of the Bank of England’s Monetary Policy Committee.

The markets are betting on UK interest rate cuts in 2024 amid recession risk, however this is only likely to reduce interest rates down to 4% – 16 times higher than the rates were only 24 months ago.

High inflation has already been felt by everyone, however the impact of the rise in interest rates is yet to bite for many; it’s set to hit 1.6 million households over the next 12 months, who have so far been shielded from the rises by low cost fixed rate deals.

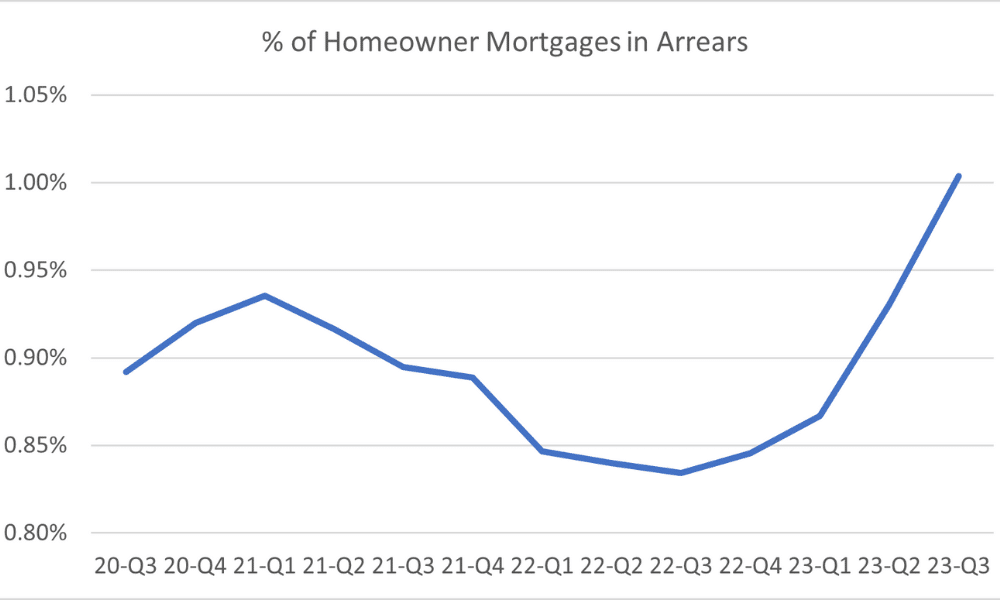

The recently published figures from UK finance show that the usual stable arrears rate on mortgages has shifted as borrowers struggle to manage repayments, with arrears rates up 20% compared to the rates seen in 2022.

This is not a problem exclusively affecting mortgage lenders. The increased cost of mortgages will have a knock on effect on the financial lives of home owners, who are likely to be seen as prime customers. With a mortgage cost increase of over £500 a month looming on the horizon for some, finances for many will be squeezed to breaking point.

Through the use of credit reference agency data cohorts, customers that could be at risk can be identified for additional intervention either at the point of taking on new credit or for those with existing credit already. The challenges for dealing with new and existing customers vary and are covered below:

New Customer Sustainability Assessment

The implications of this impending increase in expenditure for individuals with a mortgage should already be factored into lenders affordability assessments, to meet the regulatory requirement set out by the FCA in CONC requirement 5.3.1

“A firm in making its creditworthiness assessment or the assessment required by CONC 5.2.2R (1) may take into account future increases in income or future decreases in expenditure, where there is appropriate evidence of the change and the repayments are expected to be sustainable in the light of the change.”

Due to the population potentially being a minority and from a risk and affordability perspective may look good today, a tailored journey for any ‘at risk’ individuals may be required to capture details when their fixed term rates come to an end – potentially backed up by open banking data to understand whether lending will be affordable long term.

Existing Customer Proactive Engagement

Consumer duty rolled out from July last year, with a high focus on the treatment of vulnerable customers with over 100 mentions in the guidance. Engaging with existing ‘at risk’ customers to understand their circumstances ahead of time, and where they may move along the spectrum of vulnerability can improve customer outcomes by highlighting the issue to the customer who may be not yet be aware of the future problems. This is especially important where credit exposure could still increase, such as credit cards, as increasing borrowing as disposable income tightens may exacerbate the problem. Engaging digitally allows it to be carried out at scale using a less intrusive approach for customers and with additional data captured help mitigate the risk and find the right solution for the customer ahead of them struggling with repayment. As financial institutions brace for the impact on struggling borrowers, personalised engagement is key to get the right outcome, dependent on the individual customer’s circumstances.

Tailored Customer Journeys

It’s already fundamental to treat customers as individuals – but when the impact of interest rate rises begins to bite, it will become even more critical.

The financial shock from mortgage rate increases will move many to a higher level of the vulnerability spectrum (likely the most vulnerable they have ever been) and under the FCA rules firms must treat the customers fairly. The FCA expects firms to identify the risks of vulnerability within their customer base and respond.

A digital customer journey can help businesses to respond to this challenge, and provides significant benefits in the following areas:

- Treating Customers Fairly

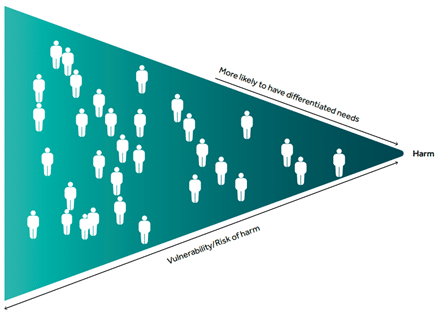

The FCA highlighted in the guidance for firms on the fair treatment of vulnerable customers that as the level of vulnerability increases so does the propensity to have differentiated needs.

A digital customer journey can be designed to dynamically adapt to each customer’s situation, applying a consistent yet flexible set of rules and treatments. Leveraging data analytics and personalisation, the journey can provide the support options to suit the unique needs of each customer to ensure they are treated fairly.

- Improved Customer Engagement

Individuals that are pushed to this new level of vulnerability may feel uncomfortable discussing their circumstances. A digital customer journey can be supportive and tailored to alleviate these concerns, allowing customers can navigate the journey at their own pace, openly sharing their financial situations without the discomfort of direct human interaction – increasing the level of engagement from customers.

- Increased Customer Value

For the customer, a tailored digital journey makes them feel valued by enhancing their experience and driving high satisfaction, enabling the business to more accurately mitigate any risks. This leads to better outcomes by reducing arrears and increasing customer retention, driving an improvement the lifetime value of a customer to the business.

- Operational Impact

Dealing with the fallout of mortgage rate rises could involve a significant operational burden, including multiple direct customer interactions, and capture of supportive evidence and complex training. A digital customer journey can reduce the operational overhead, providing customers with a way to self-service in a single process – minimising the strain on operational resources.

A Strategic Boost

Highly personalised customer journeys result not only in improved customer and commercial outcomes, but can also serve as a highly strategic brand differentiator within a crowded market. A customised journey can help the customer to feel more valued, fostering trust and loyalty.

With a £200,000, 25 year mortgage expected to increase by £495 per month, customers that are rightly worried about the effect that the interest rate rise is going to have on their mortgage repayments will greatly appreciate tailored advice and solutions – making them feel like their lender genuinely cares about their circumstances. This trust and loyalty both increases the long term value of customers, and increases the chance of positive word-of-mouth recommendations.

Personalised journeys also act as a reason to choose one institution over another. Nowadays, the majority of customers are digitally savvy and expect personalisation to make them feel valued. In a highly crowded financial market, if one organisation offers that personalisation, it serves as a distinct competitive advantage that sets it apart from the rest.

The PrinSIX Approach

PrinSIX’s solutions are purpose-built to integrate with existing technologies to react to this emerging affordability challenge at scale, alongside existing systems which may not be able to be changed in time to deal with the challenge – especially when the change is prioritised against other IT backlog items that may not get to the top of the list due to the short term nature of the problem, which only a proportion of customers are facing along with the unknown consequences in terms of business and customer outcomes. Our automated, highly personalised journeys understand each individual customer’s circumstances and drive the best results, reducing the risk of missed payments, defaults, and poor outcomes for both customers and financial institutions. Financial institutions that leverage these capabilities today can demonstrate accountability in the face of growing regulatory scrutiny over affordable lending practices.

PrinSIX’s technology allows our clients to gain a maximised understanding of each individual customer, with minimal customer friction. Through faster engagement and a frictionless digital journey, we drive better customer engagement and faster resolution – resulting in better customer outcomes.

To Sum Up

As consumers are faced with 5.25% interest rates, it’s critical that financial institutions are able to provide individual customer journeys at scale in order to meet the expectations of the regulator and support their customers. As many consumers face a significant squeeze on finances, it’s vital that organisations are able to identify customers at risk and offer tailored advice and solutions to mitigate the risk of non-payments and defaults.

Highly personalised customer journeys improve business decision making and efficiency, and reduce financial risks, without any friction. Serving as a strategic competitive advantage, offering a personalised digital journey and increasing customer satisfaction is a powerful means to maximising both customer and commercial outcomes in the face of a significant rise in interest rates.